Additive Manufacturing

Environmental Relevance of the Additive Manufacturing Industry

Each year, over 2.5 billion tons of industrial metals and plastics are processed into parts and other manufactured goods across end use sectors.

Additive manufacturing (AM) is the industrial-scale, full-process application of layer-by-layer material addition to create parts. It is the large-scale equivalent to 3D printing, which typically refers to the more consumer-focused, small-scale version of the process. In parts fabrication, the production process largely dictates what can be designed. When using conventional methods, this frequently results in heavier geometries, lower performance, and higher waste than the ideal part might allow. Each year, over 2.5 billion tons of industrial metals and plastics are processed into parts and other manufactured goods across end use sectors, with steel and plastics alone accounting for the vast majority of volumes. This scale of material transformation drives significant energy use and waste generation, underscoring the need for more resource-efficient alternatives. AM addresses these challenges by enabling near-net-shape production, minimising scrap, and allowing novel component designs that maximise performance while minimising material input.

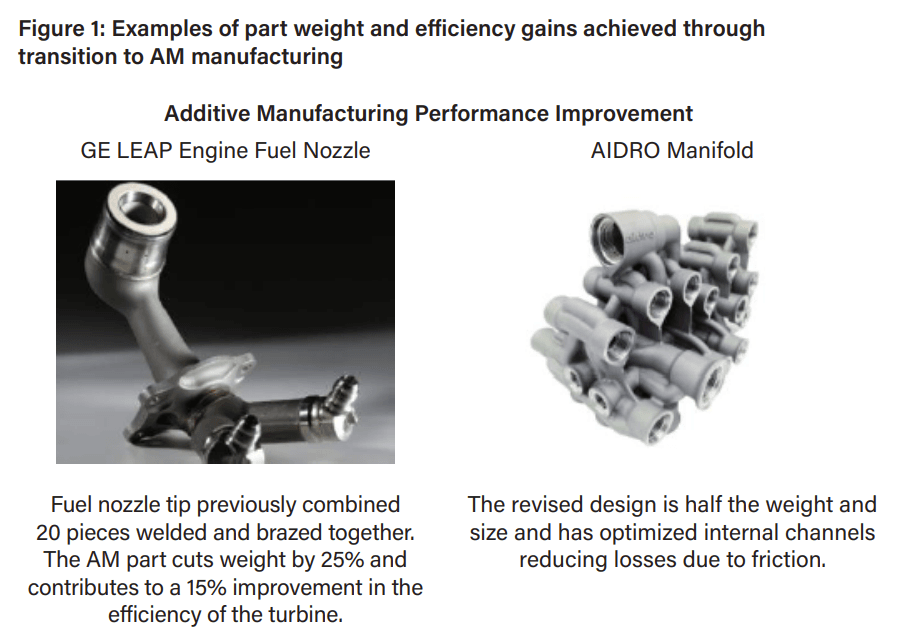

Early experiments with AM date back to the 1970s, with the first commercial systems emerging in the 1980s and 1990s for polymer-based prototyping. In this application AM was often more economical and sustainable for small runs, since parts could be produced directly without the need to produce unique moulds. By eliminating this tooling requirement, AM reduced both material use and lead times, laying the groundwork for its wider adoption. As AM matured through the 2000s, its use expanded into the production of finished parts. Contemporary AM technologies can be divided into seven families, though two dominate: Powder Bed Fusion (PBF), in which layers of powder are selectively melted by a laser or electron beam (the leading approach in metals), and Material Extrusion (MEX), in which polymers are deposited layer by layer from a heated filament. Today, these AM technologies are increasingly deployed across high-performance sectors such as aerospace, automotive, medical implants, and consumer goods, where they are displacing conventional casting, forming, and subtractive methods. When compared to these techniques, AM offers greater freedom in part geometry, allowing novel, lightweight component geometries (Fig.1). It also offers the ability to manufacture “near-net”, avoiding the material waste and associated energy consumption of machining a component from a billet.

AM offers the ability to manufacture “near-net”, minimising material waste and associated energy consumption.

These drivers have shaped the structure of the AM market today. While polymers still account for the majority of printed volume, metals represent the fastest-growing segment by value, driven by adoption in aerospace, medical implants, and high-performance automotive, in which the lightweighting achievable through AM can lead to considerable cost savings. The material use efficiency of AM is also a competitive advantage in these sectors given the cost of special alloys used.

Despite broad alignment with environmental principles of resource efficiency, AM has its own unique profile of environmental impacts which must be considered holistically when evaluating the benefit of any substitution.

Metal AM commonly makes use of specialised powders as raw feedstock, which require significant energy to process from pure metal billet (arising from both melting and atomisation steps). Accordingly, the embedded emissions per ton of metal powder are higher than for the billet that would provide the input to conventional subtractive manufacturing. Whether the material savings achieved through AM are enough to overcome this differential depends on the specific geometry of the part in question.

Similarly, while the AM process itself does away with the energy intensity of machining a part from a billet, it presents its own challenges. Perhaps most obvious among these is the energy cost of having to melt the feedstock repeatedly as the part is built up layer-by-layer. This is particularly relevant for aluminium powders, which absorb only a small fraction of the incident laser beam and so require higher energy input.

Another major contributor to the environmental footprint of metal additive manufacturing—particularly when including powder production—is the use of inert gases such as nitrogen

or argon to maintain a non-reactive atmosphere and prevent oxidation or ignition of the powder. Across the full process chain, the energy and emissions embedded in gas production and use can represent a substantial share of total energy consumption,

making it essential to evaluate environmental benefits on a case-by-case basis.

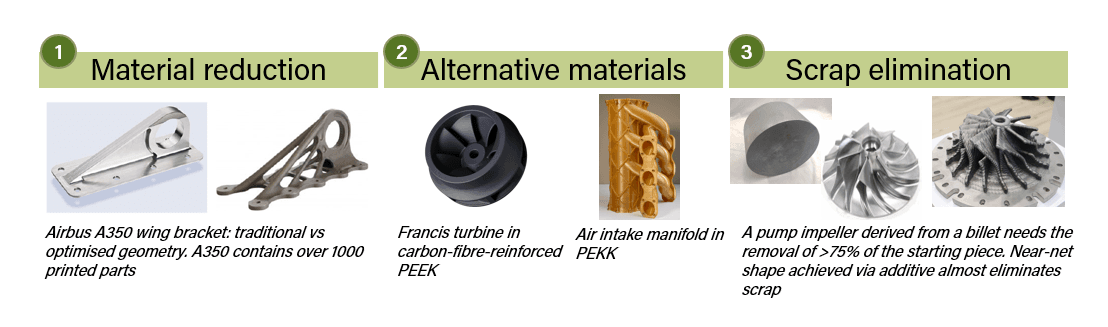

AM delivers performance and sustainability gains across three core areas:

1. Material Reduction: Topology optimisation allows parts to be designed with only the material needed, often reducing input requirements by 20–50% and sometimes by as much as 80%. Lighter parts can lower costs and improve downstream efficiency.

2.Alternative Materials: High-performance polymers and composites are more easily produced with AM than with injection moulding, where tooling costs can be prohibitive. These materials offer corrosion resistance, electrical insulation, and significant weight savings.

3. Scrap Elimination: Subtractive processes such as milling waste large volumes of material, with aerospace “buy-to-fly” ratios as high as 20:1 (only 5% of the billet ending up in the final part). By contrast, AM is nearly scrap-free which is especially relevant for complex geometries.

Additional environmental benefits can be achieved as a result of AM’s avoidance of many of the less-obvious externalities of subtractive machining such as high energy intensity from auxiliary systems and idle time, and heavy reliance on consumables such as coolants, lubricants, and cutting tools. While each scenario merits independent assessment, Ambienta’s Environmental Impact Analysis identifies benefits most strongly aligned with the taxonomy metrics Material Saved, CO2 Emissions Reduced and Pollutants Avoided.

Investment opportunities

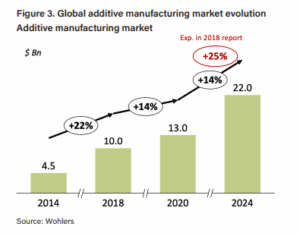

The additive manufacturing market has expanded rapidly, growing c. five-fold over the past decade.

The additive manufacturing market has expanded rapidly, growing almost five-fold over the past decade to reach a value of around $22 bn in 2024 (Fig. 3). This corresponds to a CAGR of ~14% between 2018 and 2024, falling short of 2018 predictions of 20%+ growth. These expectations drove an explosion in investments in the sector, from less than US$ 1bn in 2018 to over US$ 4bn in 2022. Investments and valuations subsequently declined as the expected growth did not fully materialise. We expect robust double-digit growth to continue in the near term, which combined with this recent market correction should provide attractive opportunities for private and public market investors.

Machine OEMs

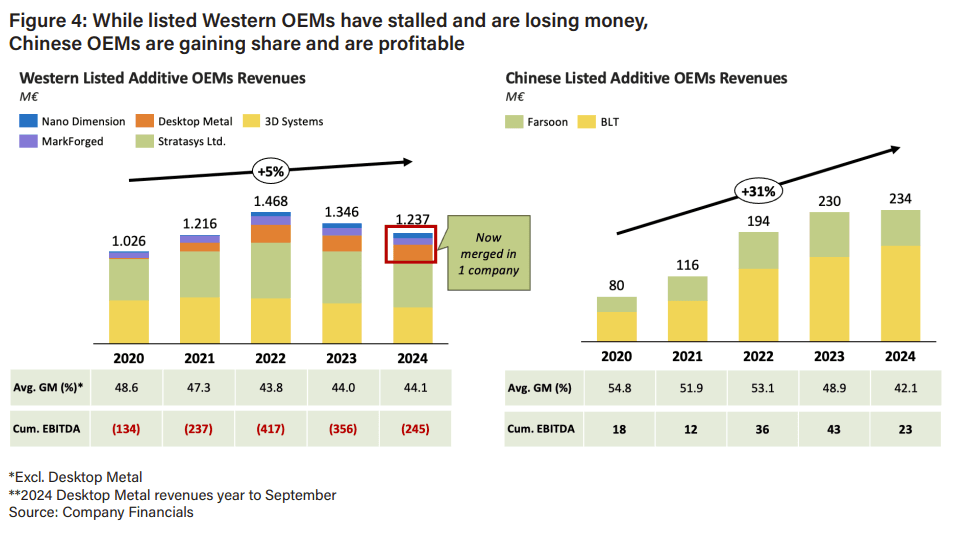

Original equipment manufacturers are companies that produce parts and equipment used in another company’s end product. While machine OEMs have been the most obvious way to invest in the AM value chain, growth ambitions often underestimated the challenges of scaling industrial capital goods franchises: long sales cycles, cyclical demand and investments in a reliable servicing network. Many players have therefore struggled with profitability, as is evident in the financials of Western-listed OEMs (Fig.4).

On the positive side, these players show healthy gross margins, and there are examples of OEMs in China that have grown revenues by over 30% annually since 2020 while maintaining positive EBITDA. We expect the industry to achieve profitability through consolidation and more discipline.

To address challenges associated with exclusively selling machines, some OEMs have decided to integrate vertically, combining machine building with materials and application expertise to sell finished parts, such Roboze, while others, such as EOS, have built consulting divisions to help customers fully leverage the potential of AM. We see service/part-oriented OEM models offering greater value creation compared to pure machine sales, as customers typically require consulting and specialist support to re-engineer parts and successfully adopt AM in production.

Large Format Additive Manufacturing (LFAM) is also emerging as a particularly attractive niche. For large, complex parts produced in low volumes, AM can be structurally more competitive than conventional methods: printing avoids the costs and long lead times of tooling for small batches. Players such as Caracol, CEAD, and BigRep are targeting this opportunity.

Post-processing solutions, which cover surface finishing, heat treatment, and machining are crucial to ensure printed parts meet industrial standards and this segment itself is evolving into a dynamic sub-market with strong value-creation potential. In fact, the cost of post-processing can be comparable to the cost of printing, and therefore automated solutions that can bring down the cost can significantly contribute to the wider adoption of additive manufacturing.

Service Bureaus

Alongside OEMs, service bureaus represent one of the most attractive areas of the value chain. Their model is supported by specialised know-how in part reengineering, the ability to handle high-complexity, low-volume jobs, and the avoidance of high upfront capex for customers. Publicly listed players such as Materialise and Protolabs combine contract manufacturing with AM-enabled design platforms, and there are multiple private equity-backed platforms in this segment.

Component Manufacturers

A further set of opportunities lies in component and subsystem suppliers, which benefit from the ongoing drive to improve speed, precision, and cost efficiency across the AM process. From laser sources and beam delivery systems to automation, continued improvements in process stability and energy efficiency, such as gas recirculation in powder production and advanced optics, represent meaningful avenues for value creation.

Material Suppliers

Finally, materials remain a critical enabler of the sector. With metals now approaching 40% of total AM material use, the demand for high-performance powders is at an all-time high. Advances in polymer chemistry and lightweighting trends are also driving growth in high-performance polymers such as PEEK, PEKK, and carbon-fibre composites. The dominance of established chemical and metallurgy groups in this space may limit the avenues for investment, though the sector remains a vital and growing part of the AM space.