Electricity Grids

Environmental problem

Electricity grids are the backbone of an electrified, low carbon economy. However, the existing grid is struggling to keep up.

The decarbonization of the energy system depends on increasing the share of carbon neutral energy production from the supply side, and on the electrification of demand, through electric vehicles, electric heat pumps and industrial processes electrification. In between demand and supply, electricity grids are the backbone of an electrified, low carbon economy. However, the existing grid is struggling to keep up:

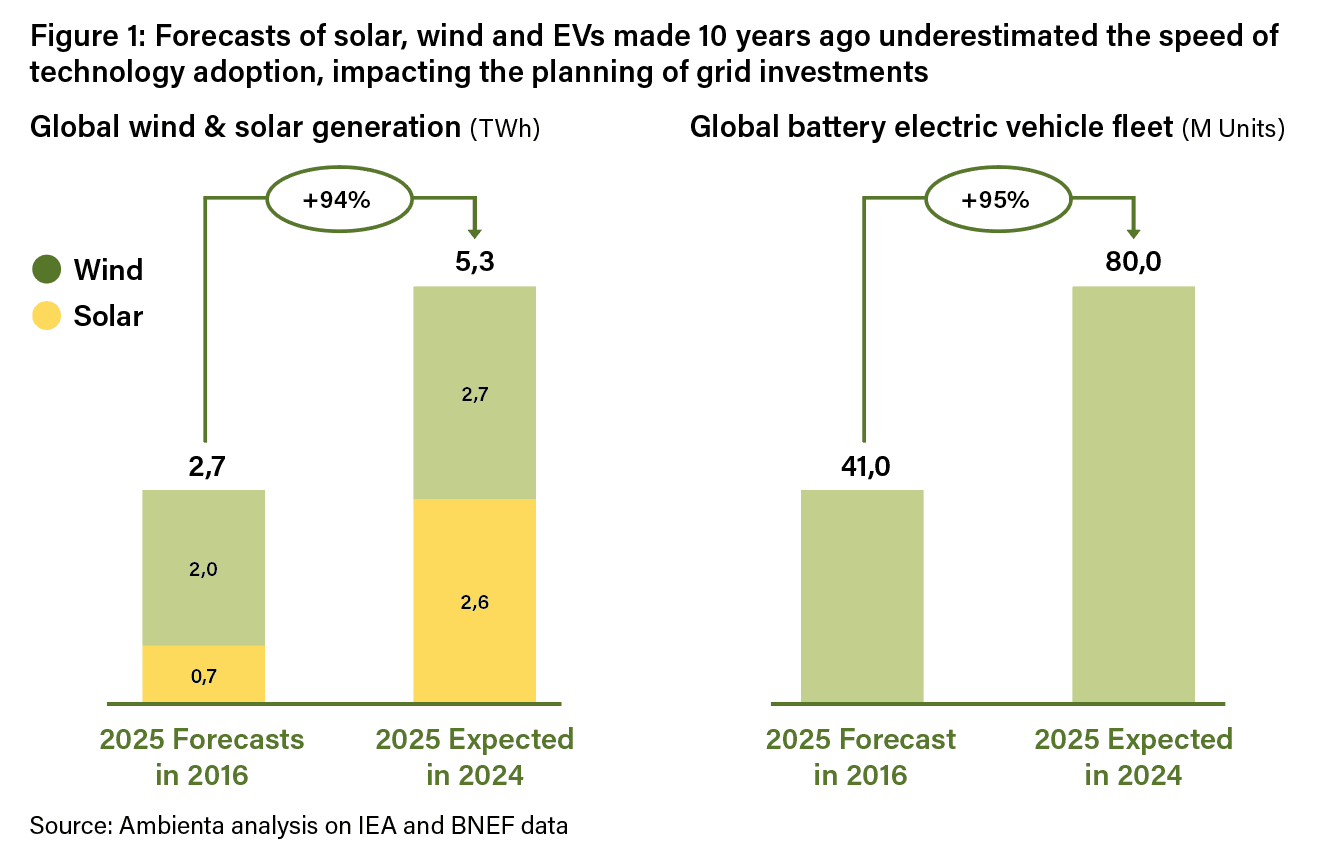

- The pace of the energy transition has been much faster than predicted in the planning horizon of grid operators. If we look at the International Energy Agency forecasts from ten years ago, the average of the 2015 World Energy Outlook scenarios indicated 2.7 TWh of wind and solar generation for 2025, while given 2024 actual data, in 2025 the world is likely to produce over 5.3 TWh of wind and solar. A similar doubling of actual figures compared to the forecasts 10 years ago can be observed in electric vehicles: the average of the scenario from the 2016 Global EV Outlook indicated c. 41 million EVs on the road in 2025, while the actual 2025 figure will likely be above 80 million vehicles. This mismatch has caused insufficient early investments in expansions from grid operators and the rise of connection queues. In the United States the average wait between applying for a grid connection and actual grid connection is now five years, double the lag seen in 2015, and at the end of 2023 there were nearly 12,000 projects representing 1.6 TW of generation capacity and 1 TW of storage awaiting interconnection. On the demand side, we have not yet reached saturation in most geographies, as existing infrastructure is able to support 15-20% penetration of electric technologies. But in places like the Netherlands where these penetrations for EVs, Heat Pumps and rooftop solar are being reached, the grid is becoming saturated, and despite a tripling of DSO investments, bottlenecks are expected to remain for the next 10 years.

- The century old infrastructure built for one way, steady flows from a handful of power stations needs to adapt to bidirectional, highly volatile currents from millions of rooftop panels, fast charging vehicles and utility scale wind farms. Roughly 40% of the European transformers were installed before 1985, many are now forced to carry loads they were not designed for. Recent events in Spain and at the Heathrow airport highlight the risks of this problem.

- Climate change poses further stress on the grid: extreme weather events and wildfires threaten the integrity of overhead cables, while rising temperatures limit the power ratings of cables and increase the load from air conditioning demands.

In summary, to support the energy transition we need a grid that is larger, smarter and more resilient, and we need it in record time.

Environmental solutions

Adapting the grid to the speed and requirements of the energy transition demands a mosaic of interventions to remove bottleneck.

Grid equipment is designed based on peak demand, but on average operate at utilizations of 50% or less.

- Maximize the utilization of existing assets: grid equipment is designed based on peak demand, but on average operate at utilizations of 50% or less. Furthermore, due to a lack of real time data, there is often a significant margin of safety embedded in the rated capacity. A variety of solutions enable the increase of energy transmitted and distributed by existing assets without the need to build new lines: real time thermal measurement of cables enables increased flows during cool conditions (“Dynamic Line Rating”); batteries on each side of a transmission line enable an increase utilization and decouple peak demand from the line power rating (“Storage as Transmission”); composite core cables can substitute legacy steel-reinforced cable on existing corridors doubling the amount of power that can be transmitted on the same infrastructure

- Expansions and reinforcements: new lines and substations remain unavoidable, as renewable hotspots are often far from demand centres: strong winds in Scotland and the North Sea in Germany need to reach London and Bavaria, and the sunny Italian south needs to power the industrial north. On distribution circuits, peak supply from rooftop PV at midday, peak heat pump demand to heat homes in the morning and the evening EV‑charging spike will also require a lot more infrastructure.

- Digitalisation and automation: real time control of what is happening on the grid, while more developed on the Transmission side, is still low on the Distribution side. Additional opportunities for optimization come from Distributed Energy Resource Management Systems (DERMS) and Virtual Power Plants (VPPs) to orchestrate behind-the-meter solar, batteries, EVs, and other flexible resources to help balance the grid dynamically.

- Flexibility: utility scale batteries, demand‑response platforms, vehicle‑to‑grid interfaces and maturing long duration energy storage solutions become more important as loads increase in variability. They cannot replace copper and steel altogether, but every megawatt shifted in time postpones or shrinks the most expensive grid reinforcements.

Investment opportunities

Globally, investments in the grid are expected to jump from c. US$ 330bn in 2023 to US$ 500‑800bn by 2030.

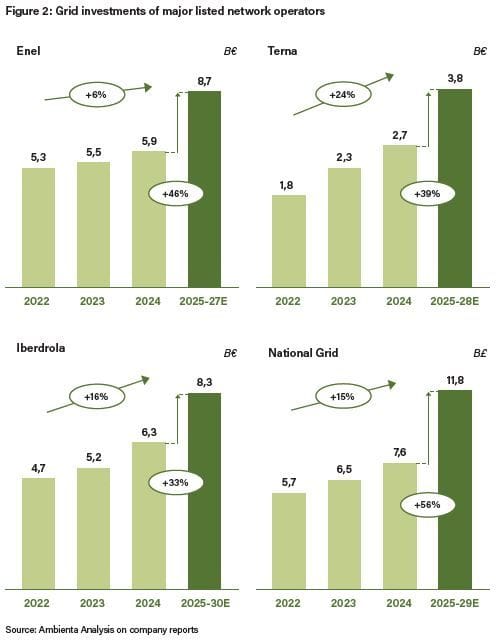

Transmission and distribution grid operators’ investment are already accelerating, and the plans of the likes of Enel, Terna, Iberdrola and National Grid foresee a further step up by 2030. Globally, investments in the grid are expected to jump from c. US$ 330bn dollars in 2023 to US$ 500‑800bn by 2030, depending on the speed of the energy transition.

We’re at the dawn of a new grid super-cycle.

For investors, opportunities arise in different segments of the value chain:

- Regulated grid network owners themselves remain attractive for income focused investors. Due to growing investments, the Regulated Asset Base of these players is expected to grow double digits for the next 5-10 years, earning a pre-agreed return. Choosing the most favourable regulatory environment in this case is they key to selecting the most attractive players.

- Equipment makers sit at the sharp end of today’s bottleneck. Large power transformers, high voltage switchgear and submarine cables enjoy multiyear order backlogs and a favourable pricing backdrop. Some technology shifts, such as the rise of high voltage direct current, the elimination of SF₆ gases and higher temperature conductors, favour established listed players with deep pockets for R&D, such as Hitachi Energy, Siemens Energy, ABB and Prysmian, but there are also some private companies leading in niches such as test and measurement instruments or insulators as well as a few innovators offering specific solutions such as TS Conductors’ composite core cables or Heron Power, the new start-up of Tesla’s former #2, working on solid state transformers.

- Services and construction firms are the unsung enablers. All players in the industry lament skilled labour shortages to face the upcoming wave of investments, with utilities increasingly outsourcing installation and maintenance to overcome bottlenecks, creating an opportunity for independent players that can effectively train, deploy and retain their technicians. In the United States, Quanta Services is a pureplay in power services, while in Europe there is a handful of diversified players such as Spie, Vinci and Bouygues, but the market is very fragmented leaving room for regional rollups.

- Digital platforms — from software to grid-edge sensor analytics—form a fast-growing pocket. Annual spending on digital grid solutions is expected to be the fastest growing category as distribution operators pivot from passive asset managers to real-time system operators. The landscape combines the established equipment providers (Siemens, Hitachi Energy), with a wave of venture-backed start-ups offering AI-driven fault detection or topology optimisation.

We’re at the dawn of a new grid super-cycle: after the buildout of the 1950s-70s to electrify households, and the second wave of development in 1990s-2000, this cycle is driven by renewables and demand electrification. Even if digitalisation and flexibility can increase the utilization of existing assets, new lines and substations as well as refurbishments and expansions of existing assets will be fundamental to future proof the grid. Companies that make, install or operate the hardware and software enabling a larger, smarter and cleaner grid will benefit from this super-cycle while enabling the energy transition, a perfect example where sustainability drives value.