Flexibility for the future of green power systems

Environmental Problem

By 2035, renewables could account for around 75% of power generation, with wind and solar output approx. 2.5x higher than today.

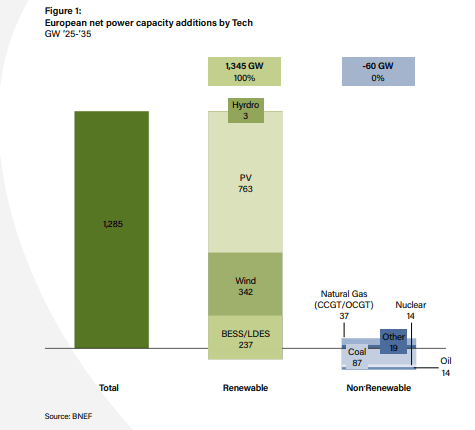

Europe is already a large, and increasingly renewable, power system, producing approximately 3,400 TWh of electricity per year, around 45% of which comes from renewables. Over the next decade, the region is expected to add roughly 1.3 TW of net new generation capacity, overwhelmingly from wind and solar. By 2035, renewables could account for around 75% of power generation, with wind and solar output approx. 2.5x higher than today. This acceleration is explicitly aimed at addressing the energy trilemma: i) providing security of supply; ii) maintaining affordability as renewables are now the lowest-cost sources of power across most of Europe; iii) achieving decarbonisation. These three objectives can only be achieved simultaneously through a power system that operates very differently from the one of the past.

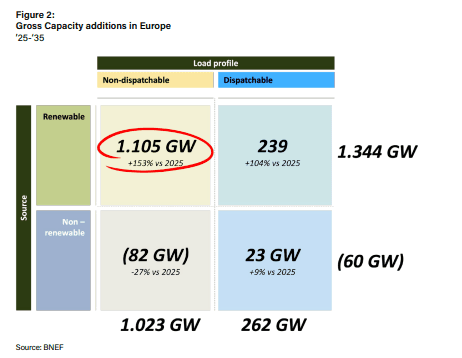

Electricity systems must be balanced in real time. At every second, supply and demand must remain in equilibrium. As the generation mix shifts towards non-dispatchable resources, meaning sources whose output cannot be adjusted in response to demand, maintaining this balance becomes both more complex and more valuable.

Two structural shifts are unfolding simultaneously:

- Supply is becoming increasingly variable. Solar and wind do not respond to demand; they depend on weather, seasonality, and daylight. This increasingly creates midday oversupply and evening scarcity, pushing prices down in certain hours ,sometimes even into negative territory, and increasing curtailment risk. In 2024, Europe recorded a record number of hours with wholesale power prices at or below zero, a clear signal of a system generating more clean electricity than it can efficiently absorb.

- Demand is becoming more electrified and more peak-oriented. Heat pumps, EV charging, data centres, and broader electrification create new load patterns, exacerbating daily and seasonal peaks.

The result is a system that needs more “elasticity” across multiple time horizons, from milliseconds to entire seasons:

- Seasonal mismatch, such as higher winter demand versus stronger summer solar output

- Daily shifting, moving energy from daytime solar peaks to evening consumption

- Intra-day imbalances, driven by forecast errors, weather volatility and short-term variability

- Frequency and stability requirements, as faster disturbances occur in a grid increasingly dominated by power electronics By 2035, along with renewable power generation, Europe’s overall flexibility need will grow. In other words: decarbonising generation is necessary, but not sufficient. Without sufficient flexibility, the system becomes increasingly exposed to curtailment, price volatility and reliability constraints, ultimately slowing the transition and increasing its overall cost.

Environmental Solutions

Flexibility is the grid’s ability to continuously rebalance electricity by shifting, storing, ramping, or reshaping supply and demand.

Flexibility is the grid’s ability to continuously rebalance electricity by shifting, storing, ramping, or reshaping supply and demand. It is not a single technology but an integrated system of assets, market mechanisms, and digital coordination, each operating on different time scales.

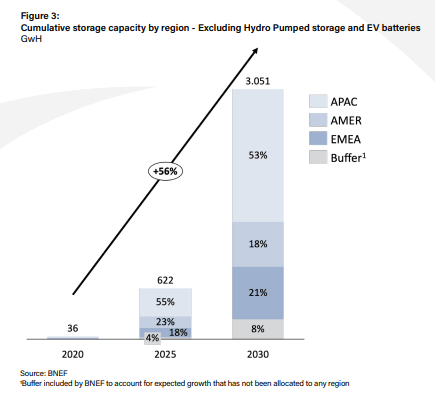

On the supply side, system flexibility covers timeframes ranging from instantaneous response to multi-day balancing. Battery Energy Storage Systems are the primary solution for seconds-to-hours balancing due to i) their extremely fast response times, ii) high efficiency and low costs (as lithium-ion battery pack prices have come down by around 93% since 2010). For longer imbalances, long-duration energy storage extends flexibility from several hours to multiple days and, in some cases, to seasonal horizons, enabling the system to manage prolonged renewable shortfalls. Throughout these extended low wind or solar periods, dispatchable generation, particularly hydro, remains essential to provide firm and reliable capacity.

On the demand side, flexibility turns electricity consumption into a controllable resource. Demand-side response allows industrial, commercial, and increasingly residential users and EV fleets to adjust consumption in response to system needs and price signals. This includes shifting industrial processes and cold storage demand peaks, optimising commercial buildings through HVAC and thermal inertia, and managing EV charging through smart charging. At the local level, distribution system operators can procure flexibility through dedicated markets to manage congestion and delay costly grid reinforcements.

Between supply and demand sits the critical orchestration layer: the aggregators and optimisation platforms which connect thousands of small loads, batteries, and distributed generators into virtual power plants, forecast availability and market conditions, and dispatch assets across wholesale, balancing, capacity, and ancillary service markets.

In practice, flexibility functions as an essential system service: a coordinated portfolio of resources that can respond at the right speed, and through the appropriate market product to keep an increasingly renewable power system stable. Multiple players and business models insist, rely, contribute and potentially even drive this transition.

Investment opportunities

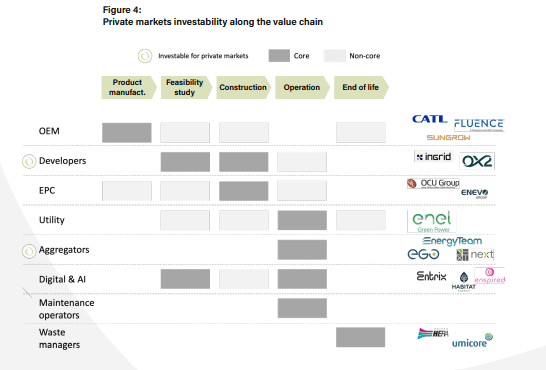

The scale-up of flexibility creates two clear and investable value pools for private markets.

The scale-up of flexibility creates two clear and investable value pools for private markets with distinct risk-return profiles and scaling dynamics. First, the build-out of energy storage. In Europe, more than 200 GW of additional storage capacity is expected to be deployed by 2035 to accommodate a much higher penetration of variable renewables. Investment opportunities are emerging along the value chain, not only in battery producers ,dominated by China, but also among EPCs and developers.

Second, aggregators and demand-side response platforms. The DSR value pool is set to expand materially by 2030 across both commercial and industrial, and residential, segments. As flexibility markets mature, scaled platforms that combine customer acquisition, optimisation and trading capabilities are likely to be structurally advantaged, enabling them to compound competitive strengths over time.

Closing thoughts

Building renewables is no longer the only bottleneck: making a renewable-heavy system work in real time is becoming equally decisive.

The energy transition is entering a new phase. Building renewables is no longer the only bottleneck: making a renewable-heavy system work in real time is becoming equally decisive. Flexibility, across storage, demand response, and digital orchestration, is what converts variable clean generation into reliable, affordable power. As the grid’s need for balancing grows, so does the opportunity to back the platforms and asset bases that will underpin Europe’s next-generation energy system.

Important information

This material is of a promotional nature and is provided for information purposes only. Please note that this material may contain technical language. For this reason, they may not be suitable for readers without professional investment experience. This document is issued by Ambienta SGR S.p.A. It is not intended for solicitation or for an offer to buy or sell any financial instrument, distribution, publication, or use in any jurisdiction where such solicitation, offer, distribution, publication or use would be unlawful, nor is it aimed at any person or entity to whom it would be unlawful to address such a document.

This material is of a promotional nature and is provided for information purposes only. Please note that this material may contain technical language. For this reason, they may not be suitable for readers without professional investment experience. This document is issued by Ambienta SGR S.p.A. It is not intended for solicitation or for an offer to buy or sell any financial instrument, distribution, publication, or use in any jurisdiction where such solicitation, offer, distribution, publication or use would be unlawful, nor is it aimed at any person or entity to whom it would be unlawful to address such a document.

Nothing in this document constitutes legal, accounting or tax advice. The information and analysis contained herein are based on sources considered reliable. Ambienta SGR S.p.A uses its best effort to ensure the timeliness, accuracy, and comprehensiveness of the information contained in this marketing communication. Nevertheless, all information and opinions as well as calculations indicated herein may change without notice.

Ambienta SGR S.p.A. has not considered the suitability of this investment against your individual needs and risk tolerance. To ensure you understand whether our product is suitable, please read the Prospectus and relevant offering documents. Any decision to invest must be based solely on the information contained in the Prospectus and the offering documentation. We strongly recommend that you seek independent professional advice prior to investing.