Low Voltage Building Products

Environmental problem

The building and construction industry accounts for nearly 40% of global greenhouse gas (GHG) emissions. Two-thirds of these emissions stem from the operational phase of buildings, including heating, cooling, lighting, and appliance use.

The technological challenges of decarbonising buildings are surmountable, despite certain constraints in their application for older buildings. We now have mature technologies available to address building emissions effectively -electrification stands out as the key solution. By electrifying all energy consumption in buildings and utilising clean electricity, we can pave a clear path toward achieving net-zero lifetime emissions for buildings.

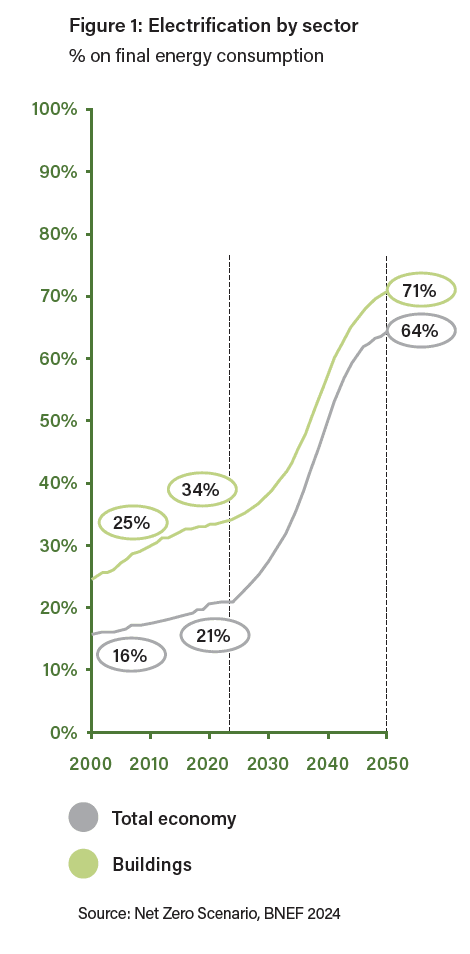

Electricity currently supplies 34% of total energy used in buildings, up from 25% in 2000, but still falls short of reaching the 70% electrification target over the next 30 years.

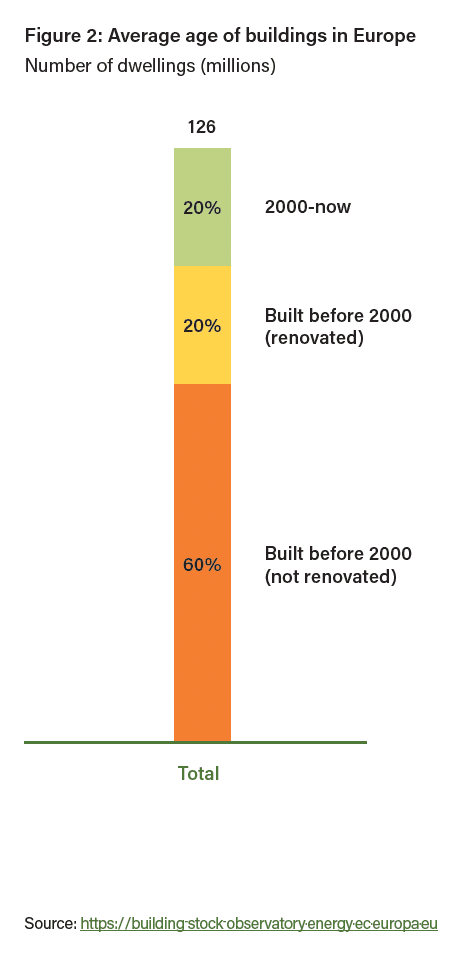

The real hurdle lies in the substantial effort required to decarbonise buildings. Currently, only 34% of building energy consumption is electrified, up from 25% in 2000, yet this pace is insufficient to meet the 70% electrification target set for the next 30 years. Moreover, in Europe, the building stock is notably aged. Approximately 80% of buildings are 20 years old or more, as such they do not meet modern electrical standards. The historical 1% annual renovation rate over the past 20 years has led to only 20% of the old building stock being upgraded to a modern level of electrification—such as incorporating solar panels, induction cooktops, and electric boilers. To upgrade the remaining 60% of old buildings by 2050, we need to at least double the current renovation rate.

Environmental solutions

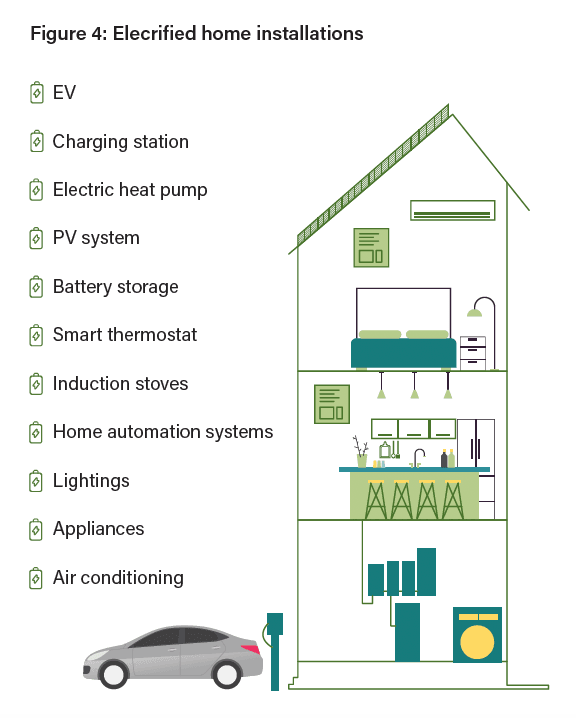

A three-step approach is crucial to decarbonising building operations. While the first step—electrifying demand—is evident, the other two are of equal importance.

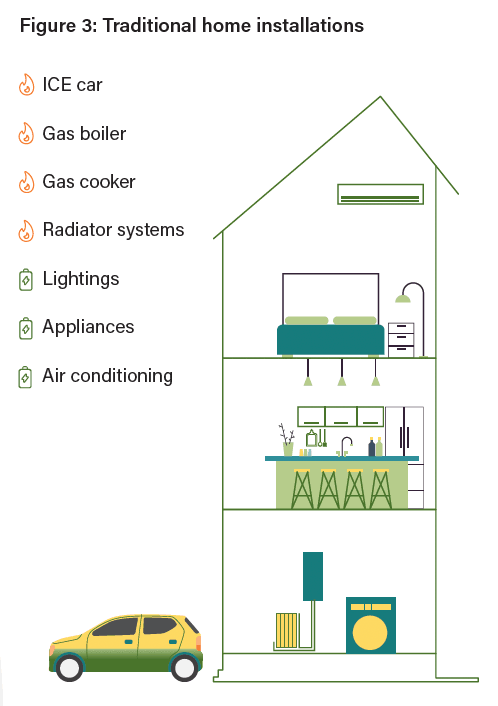

- Electrifying Demand. Upgrading to all-electric appliances and heating/cooling systems to eliminate fossil fuel use in buildings is key. This includes adopting induction cooktops, electric water heaters, heat pumps, and electric heating systems. Combining these with solar panels, where feasible, enhances daytime electricity generation and helps to normalise energy costs.

- Automation and Control. Although less obvious to the public, automation systems are gaining traction, especially in commercial buildings, due to their limited investment requirements and high payoff. For instance, Belimo, a leading producer of HVAC control devices, reports that investing in its products can yield a payback period of less than two years (equivalent to a 40% internal rate of return if considered a financial investment). The ISO 52120-1:2021 standard—a general framework for building automation and control—demonstrates that achieving a high degree of automation (Class A according to the standard) can result in over 50% energy savings.

- Increasingh Safety and Reliability. Relying solely on electricity raises concerns about resilience. To address this, buildings can incorporate battery storage systems to sustain operations during power outages. Additionally, isolating different electrical systems within a building ensures that a fault in one does not compromise the entire system.

“A three-step approach is essential to decarbonising building operations: electrify 100% of energy demand, implement automation, and enhance system reliability.”

Investment opportunities

The electrical equipment market is a $1.5 trillion industry, roughly half the size of the automotive sector. It is expected to grow rapidly, surpassing GDP growth with an anticipated compound annual growth rate (CAGR) of approximately 6–10% thropugh to 2030, driven by the global push for electrification. This swift growth also results from market commoditisation in several segments, such as energy generation, energy storage, lighting, and general appliances. Investors should focus on segments that not only exhibit rapid growth but also possess competitive advantages that create barriers to entry, thereby protecting or even enhancing profit margins. Key investment opportunities include:

- Manufacturers of Low-Voltage Control and Safety Equipment. The electrification trend increases demand for control and safety equipment like circuit breakers, switchgears, relays, sensors, and wiring accessories. These “behind-the-wall” components are technical purchases made by electrical installers based on specifications, reliability, and brand reputation. Demand for these items is inelastic, driven by necessity rather than price sensitivity. Consequently, companies can employ markdown pricing strategies, allowing for price increases above inflation and improved margins.

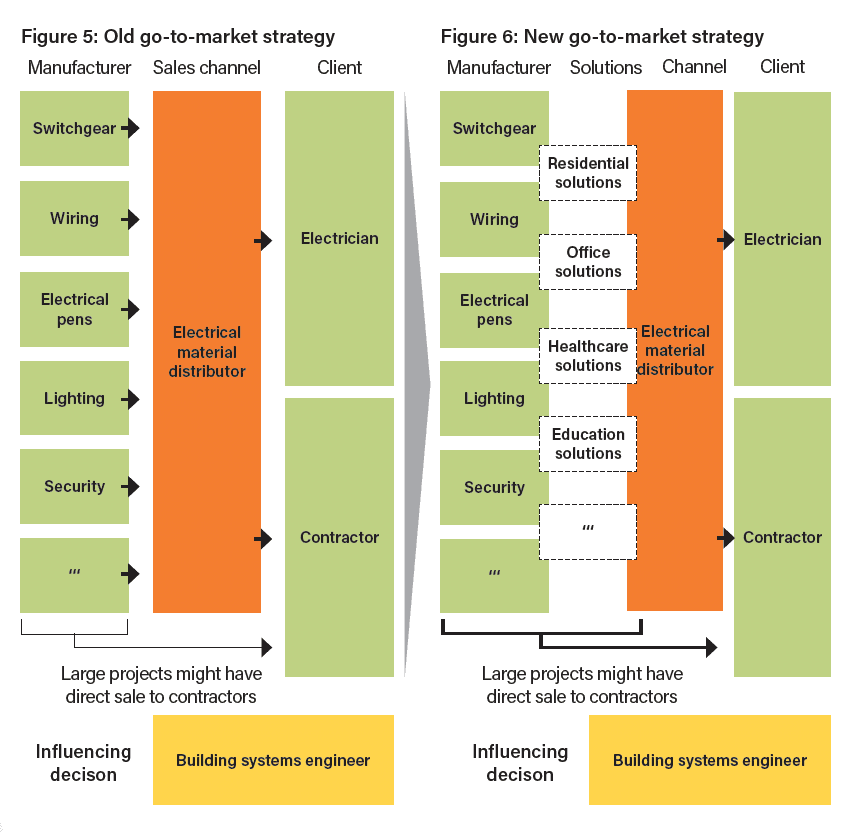

- Transformation of Distribution Channels. As low voltage building products and systems grow more complex, installers may struggle to stay updated with the latest technologies. Distributors can capitalise on this by enhancing their value proposition—offering bundled products and solution-based sales to installers. Electrical product distributors are increasingly featuring thematic areas in showrooms, staffed by specialists who consult on innovative solutions like integrated solar and heat pump systems or advanced home automation.

- Electrical Installers. Installers represent a critical bottleneck in the electrification process, potentially more so than the demand for low voltage building products themselves. Countries like Italy, the UK, and those in the Nordic region face a significant shortage of installers, driven by heightened electrification demand and an aging workforce. The installer market is highly fragmented, with many small firms unable to manage the growing complexity of modern systems. Larger contractors that can consolidate the workforce, optimize operations, and provide comprehensive training are positioned to achieve growth rates exceeding the market average.