Reusable Transport Packaging

Environmental problem

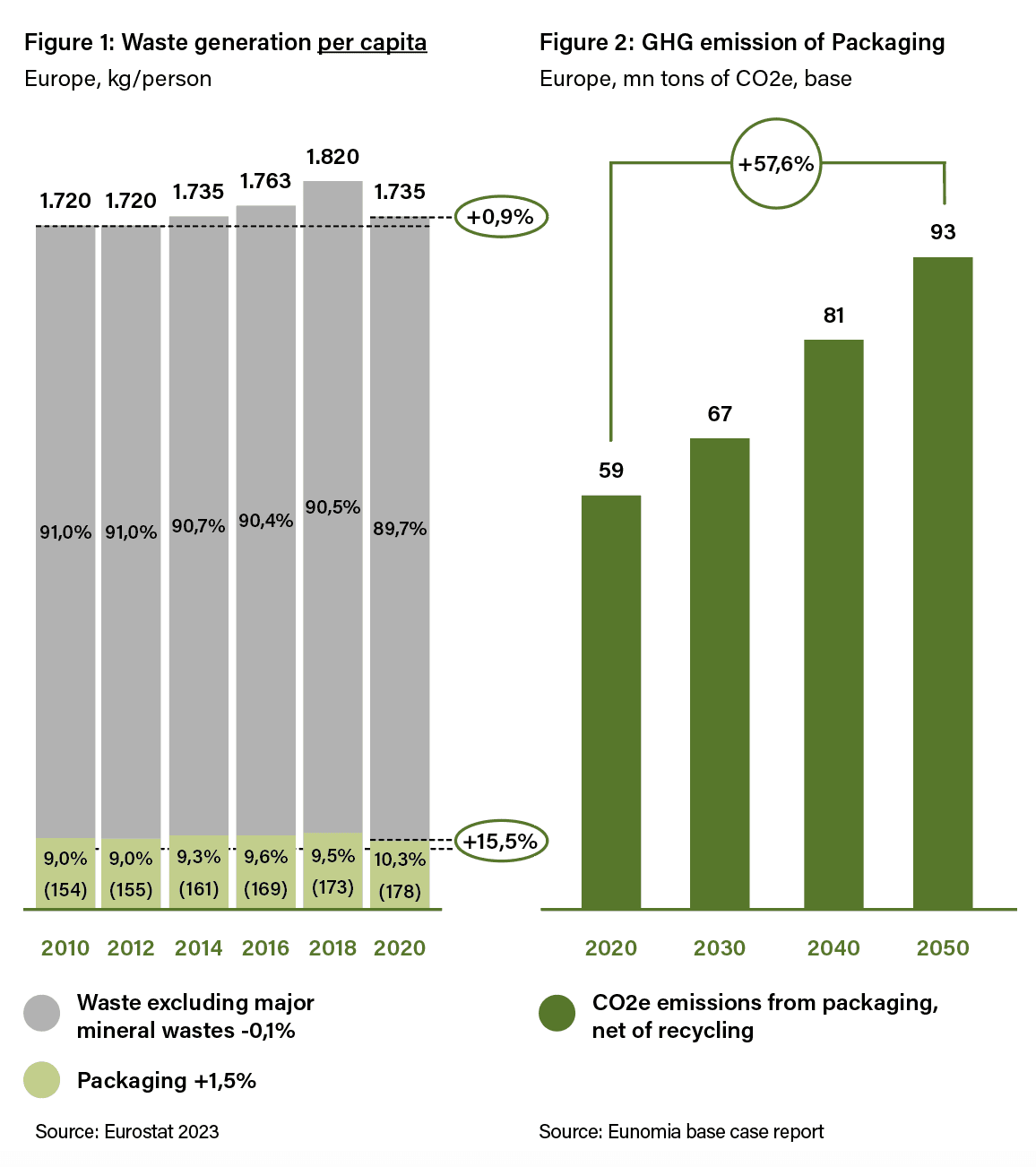

In the last decade, packaging waste per capita in Europe has surged by 15%, outpacing other waste categories. In 2020, each European citizen generated 178kg of packaging waste annually, that is 24 kg more than ten years prior.

If this growth continues alongside current recycling trends, greenhouse gas emissions from packaging are set to rise sharply. In 2020, packaging-related GHG emissions reached 59 million tonnes and are projected to hit 93 million tonnes by 2050.

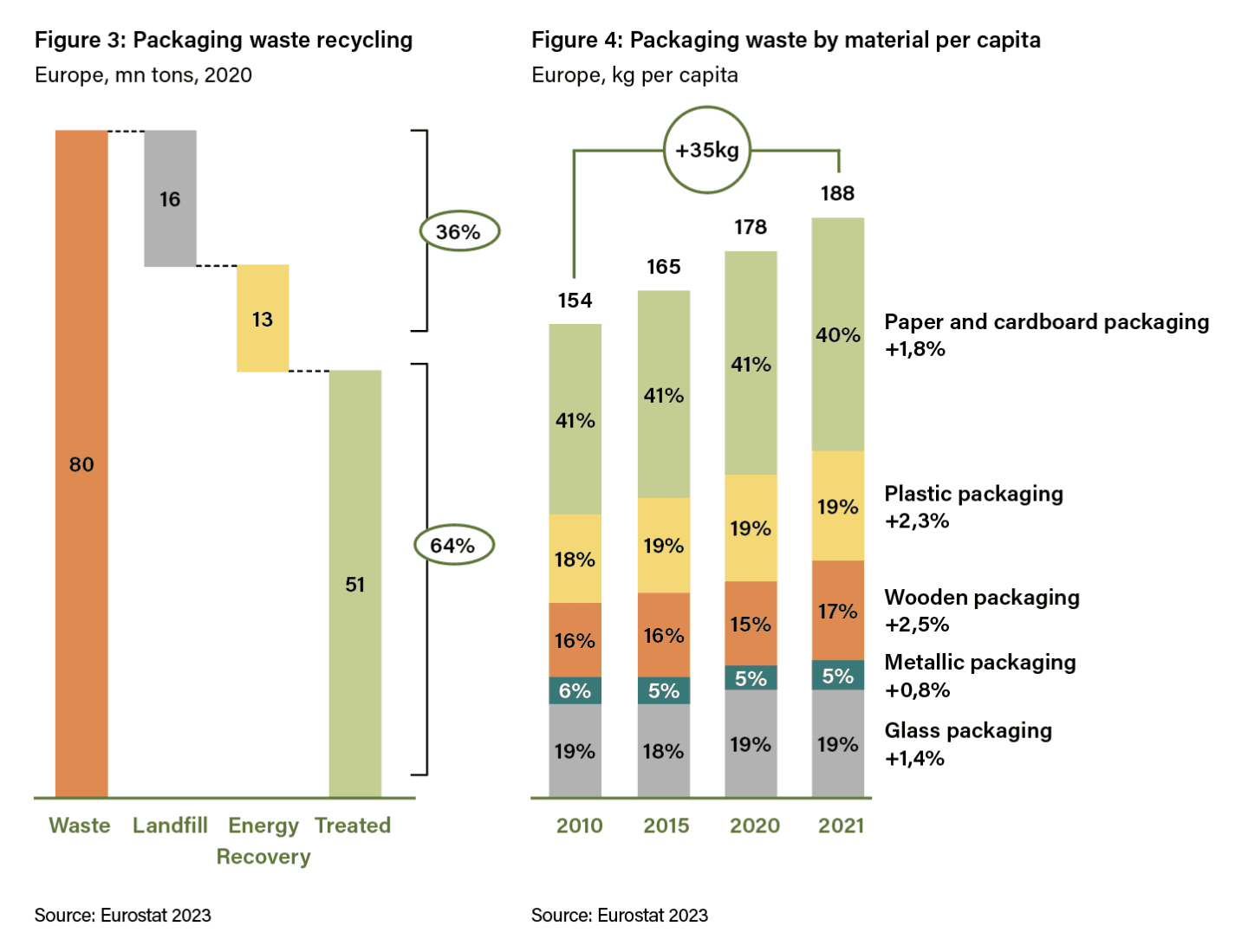

“36% of packaging in Europe ends up in landfill or is incinerated.”

Furthermore, just over half of packaging waste in Europe is adequately treated, with over a third ending up in landfill or being incinerated, both of which are less favourable than recycling. Beyond landfill and incineration, worth noting also that littering remains unaccounted for in data and adds to the list of packaging waste issues still short of a solution.

Within packaging waste, paper and cardboard account for 40% of packaging waste by weight, but plastics and wood are driving the per capita increase, growing faster than other materials.

Packaging waste is evenly divided between primary packaging, which encompasses products like bottles and boxes, and secondary packaging, used for grouping, such as larger cartons or pallets – which is the segment we focus on in this article as transport packaging.

While paper and cardboard packaging already use high levels of recycled material, the use of recycled plastic in production remains limited. For the 61 million tons of plastic products produced in Europe, only 16% of feedstock used was recycled. Packaging consumption in Europe is growing and while increasing recycling is crucial, additional solutions are necessary to address the issue more effectively and promptly.

“In Europe only 16% of plastic used in products comes from recycled materials.”

Environmental Solutions

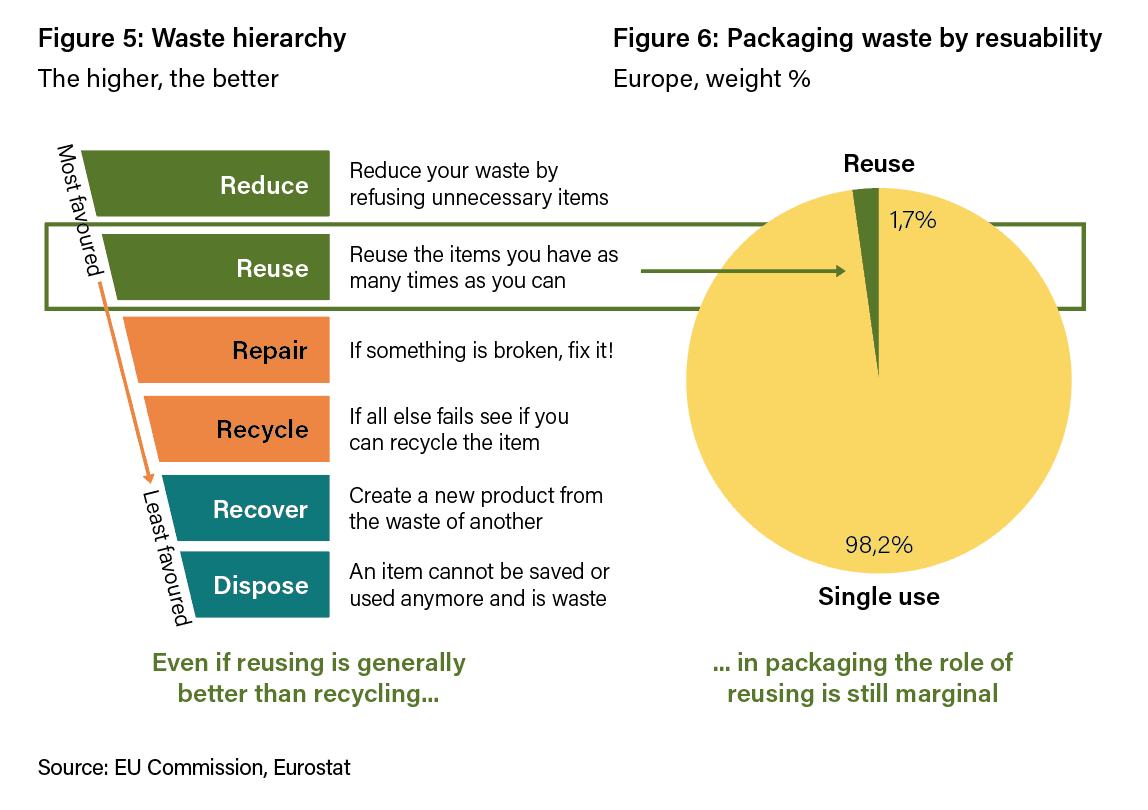

Waste reduction through reuse can complement recycling efforts. Reusing durable packaging is typically (but not always) more environmentally friendly than recycling single-use alternatives. However, reusable packaging has seen Examples of reusable packaging range from widely used wooden pallets to rigid plastic containers used in food, automotive, and other industries. limited adoption, mostly confined to specific niches where the business model is well-established and accepted by all value chain participants. Today, in terms of waste, reusable options only represent 1.7% of total weight.

“Reusing durable packaging is typically more environmentally friendly than recycling single-use alternatives.”

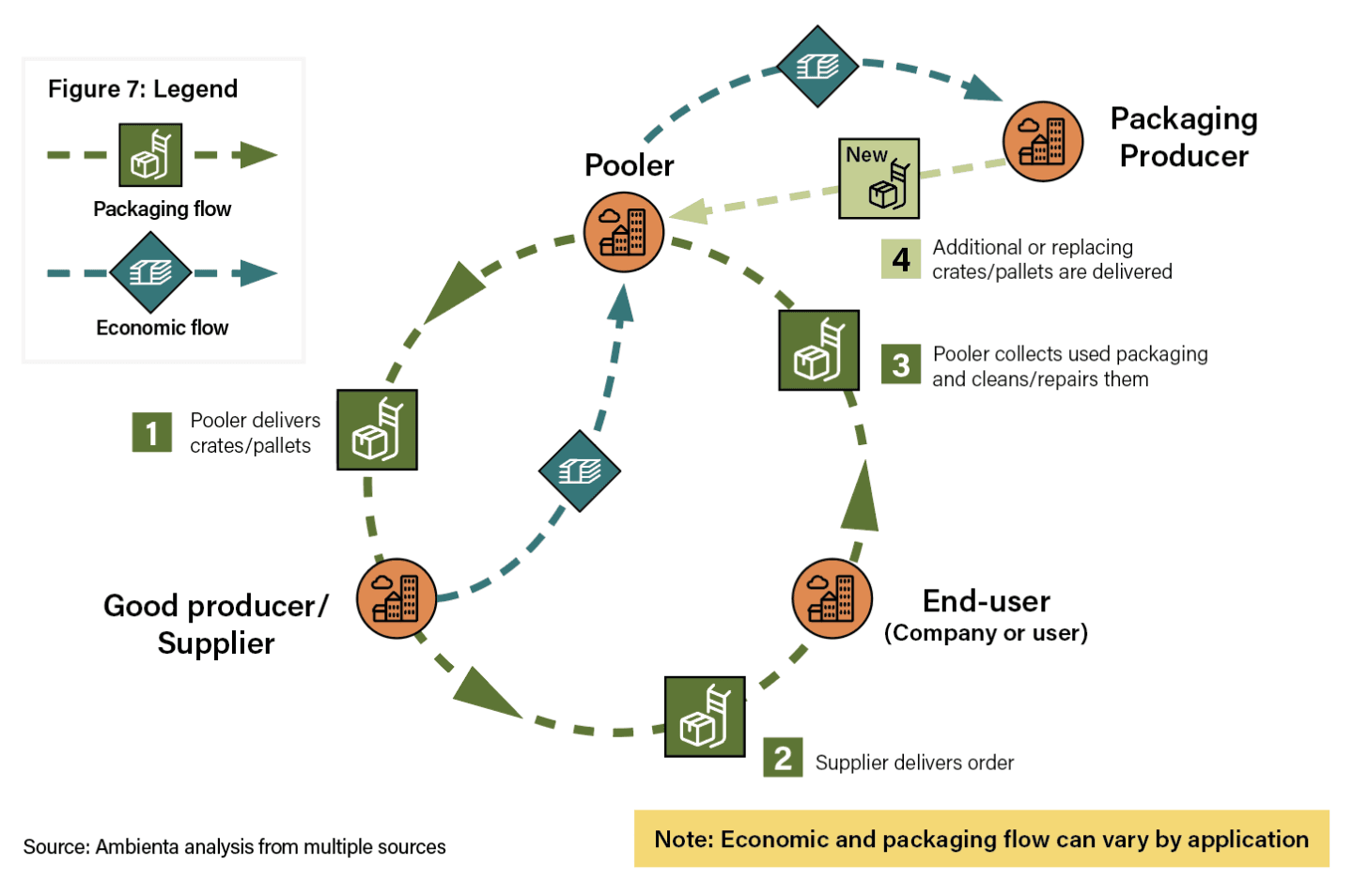

Examples of reusable packaging range from widely used wooden pallets to rigid plastic containers used in food, automotive, and other industries. These solutions often require a thirdparty pooler to manage the logistics of packaging assets. The pooler usually owns the assets and charges a fee per use.

Despite its potential, reusable packaging remains a niche market servicing specialised market segments and is most developed in fast moving consumer goods. The food and beverage sectors have adopted reusable packaging more widely, while other sectors are still in the early stages of adoption. Drivers promoting the adoption of reusable transport packaging include economic, regulatory, and client preference factors:

Economic drivers: In mature niches, economies of scale and concentration of player at the end of the value chain have improved the competitiveness of reusable packaging. This is seen in sectors like food retail, fast-moving consumer goods (FMCG), and automotive, where items like pallets and crates are widely reused.

Regulatory drivers: The EU Packaging and Packaging Waste Regulation (PPWR) sets reuse targets for specific packaging types, ranging from 10% to 40% by 2030. However, certain exemptions apply based on material, such as cardboard, or distributor size. Member states with high recycling performance may also receive flexibility in meeting reuse targets.

Client preference drivers: Demand for reusable packaging is increasing also due to demand in automated warehouses where high-quality packaging is necessary to prevent mechanical processing failures . Additionally, as more companies set decarbonisation targets, reusable packaging solutions are becoming more attractive. Consumers can be also sensitive to the topic, at least as long as price

do not harm too much.

It is worth noting that an ongoing debate persists around the sustainability of reusable packaging against the backdrop of recyclability of single-use cardboard or the lightweight nature of some plastic packaging. While academic studies generally indicate that reusable packaging represents the most environmentally sustainable solution to single-use alternatives, this conclusion must be assessed on a case-by-case basis. We must also acknowledge the fact that we see lobbying efforts, especially from industry associations, financing studies in support single-use packaging.

Investment opportunities

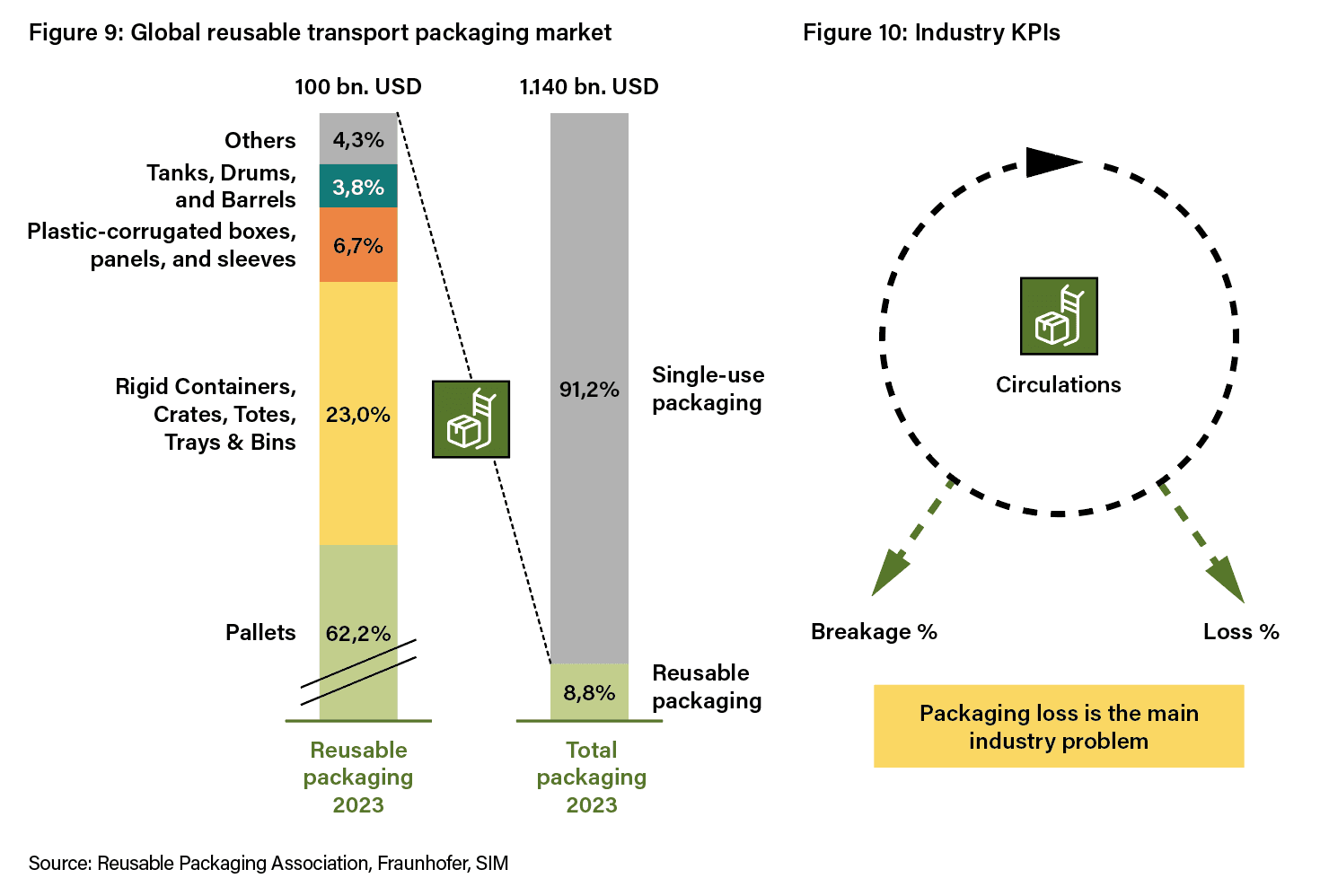

Despite a niche within packaging as a whole, the reusable packaging market is already a $100 billion industry, dominated by reusable pallet solutions which today represent more than 60% of the market value. This market is set to grow at more than 5% per year in the medium term.

Mature solutions demonstrate high performance on the key performance indicators of the industry:

- Circulation rate: Number of packaging reuse before disposal.

- Loss rate: Percentage of reusable packaging lost during a circulation.

- Breakage rate: Proportion of reusable packaging damaged during a circulation.

These KPIs are vital for economic and environmental sustainability, with application in sectors in which reusable packaging is more widely adopted typically demonstrating strong performance. For example, a crate in the mature market of reusable fruit and vegetable crates in the retail sector can be used up to 50 times, while nascent solutions like reusable e-commerce packaging struggles to reach two circulations.

As a result, investment opportunities can lie in poolers with established positions and high circulation rates. However, client concentration and capital expenditure need for packaging fleets must also be considered when assessing investment opportunities.

The most prominent company in this area is Brambles, a global publicly listed player in pooling and managing reusable pallets and containers in over 60 countries. Beyond this we see investment opportunities in niche reusable packaging producers for the food and beverage sector, as well as service providers specialising in cleaning and logistics.

In summary, reusable transport packaging complements waste reduction efforts and, together with recyclable paper and cardboard, is set to enhance the sustainability of the packaging industry.